Freight Broker Insurance Explained for Texas Crashes

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- The $75,000 surety bond that federal law requires freight brokers to maintain covers freight industry financial obligations. It does not cover personal injury claims by crash victims.

- A freight broker faces direct liability for negligent carrier selection when it hired a carrier without adequately checking that carrier's safety record, licensing, or prior crash history.

- The U.S. Supreme Court's 2024 decision in Montgomery v. Caribe Transport confirmed that state-law negligent selection claims against freight brokers are not preempted by federal law, giving Texas crash victims a viable path to broker liability.

You were injured in a crash involving a commercial truck and you have learned that the load was arranged by a freight broker. You want to know whether the broker can be held responsible and what insurance, if any, they carry. The answer is more nuanced than most victims expect: the broker’s required federal bond does not cover your injuries, but a different legal theory and a recent Supreme Court decision may give you a direct path to broker liability.

What a Freight Broker Does and How They Connect to a Truck Crash

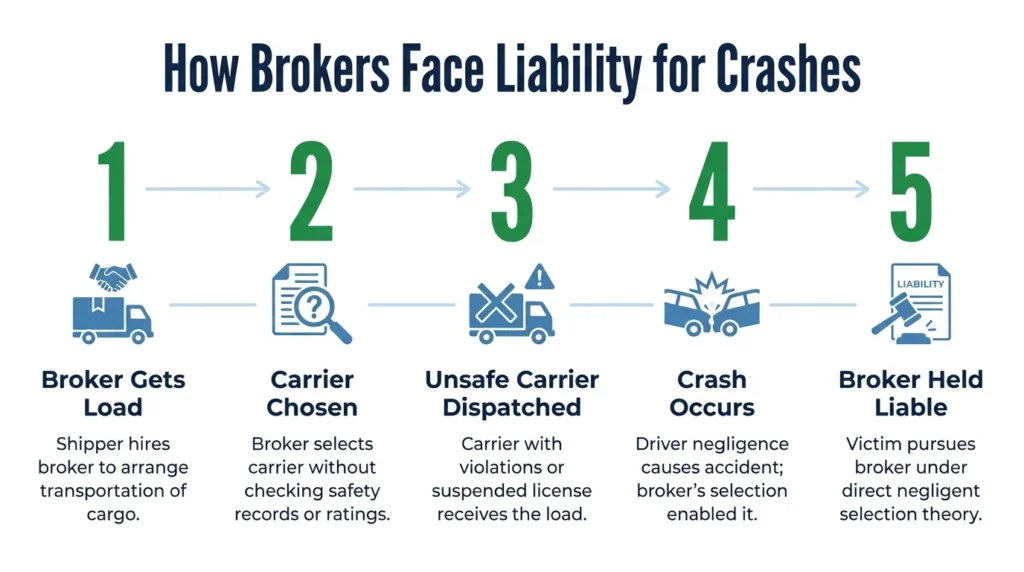

A freight broker is an intermediary. It arranges transportation between shippers (companies that need goods moved) and carriers (trucking companies that own the trucks and employ or contract the drivers). The broker does not own the truck that caused your crash. It does not employ the driver. It does not touch the cargo in transit.

Because the broker does not control how the driver operates the truck on the road, traditional vicarious liability does not apply to the broker for the driver’s negligence. The motor carrier faces that liability directly. The broker’s liability runs through a different legal theory: the broker’s own choice of carrier.

If the broker chose a carrier it knew or should have known was unsafe, because of prior crashes, a poor safety rating, or regulatory violations that were publicly available, the broker is responsible for that selection. The driver caused the crash; the broker chose the driver’s employer. Both choices have legal consequences.

Understanding how commercial truck insurance requirements work provides context for how the motor carrier’s coverage and the broker’s potential liability interact.

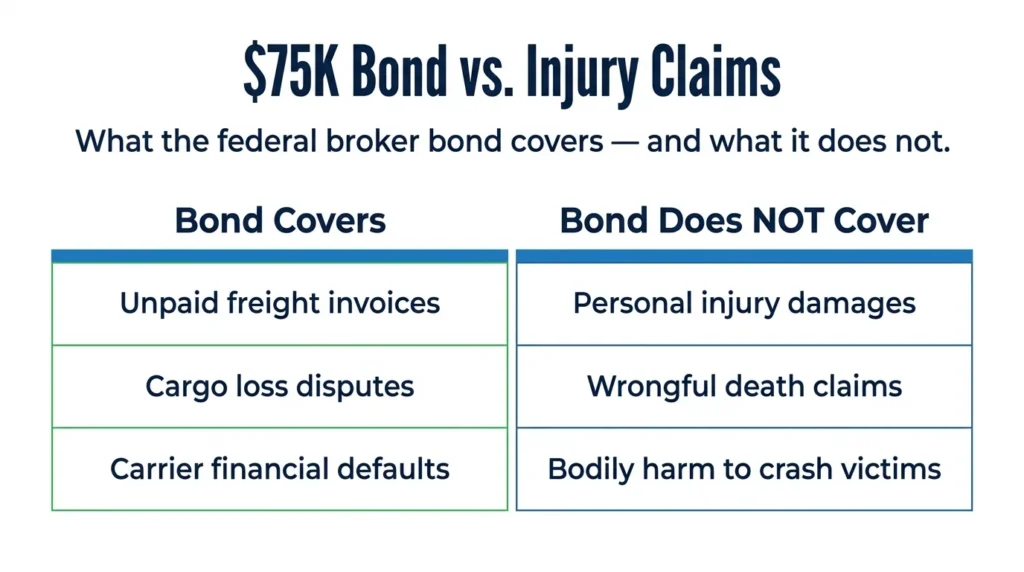

What the $75,000 Federal Bond Covers and What It Does Not

Federal law requires licensed freight brokers to maintain one form of financial security: a $75,000 surety bond or equivalent trust fund. That requirement is codified at 49 CFR § 387.307, and it is the only federally mandated financial responsibility obligation for brokers.

The bond is not liability insurance. It is a financial instrument designed to protect motor carriers from unpaid freight charges and shippers from cargo losses, the commercial disputes that arise in freight logistics. The regulation that requires the bond is about freight industry financial reliability, not about compensating people who are injured in crashes.

A crash victim cannot collect from the $75,000 bond for personal injury or wrongful death damages. The bond does not respond to bodily injury claims at all. Federal law does not require freight brokers to carry bodily injury liability insurance of any kind. A broker operating in full compliance with federal requirements may have no policy at all that responds to a personal injury judgment.

The $75,000 bond protects freight carriers from unpaid invoices, not people injured in crashes the broker helped arrange. Broker liability for victims runs through a different legal theory entirely.

How Negligent Carrier Selection Creates Direct Broker Liability

A freight broker has a duty of care in selecting the carriers it hires. Before tendering a load to a carrier, the broker must exercise reasonable care to verify that the carrier is properly licensed, maintains required insurance, and has an acceptable safety record.

What reasonable care looks like in practice: checking the carrier’s profile on FMCSA’s SAFER database, which is publicly accessible and contains each carrier’s safety rating, crash history, out-of-service rate, and inspection record.

A carrier with an Unsatisfactory safety rating is not qualified to haul loads under federal regulations. A carrier with a pattern of recent out-of-service violations is flagging safety problems that any diligent broker should notice.

When a broker hires a carrier without checking that record, or hires a carrier despite a documented history of violations, the broker’s failure to screen is the negligent act. The claim against the broker is not that the broker drove carelessly; it is that the broker chose carelessly. The driver’s negligence caused the crash. The broker’s negligence put that driver on the road with that load.

This distinction matters for recovery. The broker’s direct liability is independent of the motor carrier’s liability. A victim can pursue both the carrier and the broker as co-defendants, each on separate legal theories, simultaneously.

Texas truck accident claims involving brokers require investigating the selection decision, not just the crash itself.

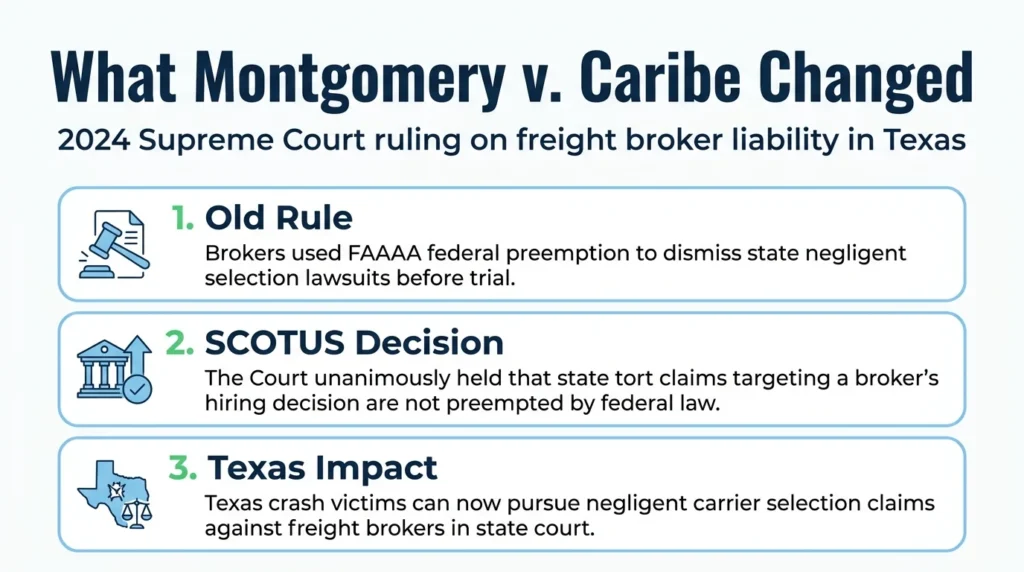

The Supreme Court Decision That Ended Broker Preemption Arguments

Until 2024, freight brokers had a powerful legal defense against state-court negligence claims. The Federal Aviation Administration Authorization Act (FAAAA) preempts state laws “related to” the price, route, or service of motor carriers. Brokers argued that a state negligence claim targeting their carrier selection decision was “related to” a carrier’s service, and therefore preempted by federal law.

This argument was used to dismiss personal injury claims against brokers in federal courts. Victims who had strong negligent selection cases found them dismissed on the grounds that federal law prohibited the state tort claim entirely.

In 2024, the U.S. Supreme Court unanimously rejected this position in Montgomery v. Caribe Transport II, LLC. The Court held that state-law negligent hiring claims against freight brokers are not preempted by the FAAAA.

A general state tort law governing a broker’s decision about which carrier to hire is not “related to” a motor carrier’s price, route, or service in the way the preemption provision requires. It addresses the broker’s own conduct, not the carrier’s operations.

The practical effect for Texas crash victims is direct: after Montgomery, a broker cannot escape accountability in Texas state court by invoking federal preemption. Negligent carrier selection is a viable claim under Texas law, and state courts can adjudicate it.

What Insurance Brokers Actually Carry and When It Applies

Some freight brokers voluntarily carry contingent auto liability insurance, also called freight broker liability insurance or contingent cargo liability coverage. This policy is designed to respond when the motor carrier’s own liability insurance is exhausted, unavailable, or denied and the broker faces a claim connected to the carrier’s operations.

This coverage is not required by federal law or Texas law. Whether a specific broker carries it is entirely a matter of that broker’s own risk management choices. Larger brokers operating in high-volume freight markets are more likely to carry this coverage. Smaller brokers may carry nothing beyond the $75,000 bond.

When the broker carries contingent auto liability coverage and the carrier’s primary insurance fails to respond, the broker’s policy provides the next coverage layer for the victim’s claim. When the broker carries no liability insurance at all, the path to broker recovery runs entirely through litigation, establishing negligent selection, obtaining a judgment, and collecting against the broker’s assets.

Understanding the timeline of a Texas commercial truck accident claim helps victims recognize when broker liability becomes part of the analysis and what investigation needs to happen early to preserve that option. Understanding how truck accident claims work in Texas clarifies where broker investigation fits into the overall claim.

Prior case results in Texas commercial vehicle matters reflect how multi-defendant claims (including claims against brokers) can resolve when the full liability picture is developed.

Work with an Injury Attorney

Freight broker liability is one of the least understood coverage questions in commercial truck crashes, and one of the most consequential when the motor carrier’s coverage falls short. Angel Reyes & Associates has handled Texas commercial vehicle accident claims for over 30 years. Our firm works on contingency: no fee unless we win. Contact us at our contact page for a free consultation.

Past results do not guarantee future outcomes.

Freight Broker Insurance FAQs

Can I sue the freight broker even if the trucking company has insurance?

Yes. The broker’s negligent selection claim is an independent theory based on the broker’s own conduct in choosing the carrier. The fact that the motor carrier carries insurance and faces liability for its driver’s negligence does not bar a separate claim against the broker. You can pursue both defendants simultaneously, and the broker’s liability does not depend on whether the carrier’s coverage is sufficient.

How do I find out if the freight broker selected a dangerous carrier?

The FMCSA’s SAFER database is publicly accessible and contains each carrier’s safety rating, inspection history, out-of-service rate, and crash data. If the carrier the broker selected had a documented history of violations or an Unsatisfactory safety rating that was visible before the crash, that information forms the foundation of a negligent selection argument. Your attorney can also subpoena the broker’s internal carrier vetting records to determine what the broker actually reviewed before tendering the load.

What did the Montgomery Supreme Court decision actually change for Texas victims?

Before Montgomery v. Caribe Transport II, LLC (2024), brokers argued that the Federal Aviation Administration Authorization Act preempted state tort claims against them for negligent carrier selection. Courts applying this argument dismissed personal injury claims against brokers on federal preemption grounds. The Supreme Court unanimously rejected the preemption argument, holding that general state tort law governing a broker’s hiring decision is not the type of state law the FAAAA was designed to preempt. After Montgomery, Texas courts can hear negligent selection claims against brokers.

Does the $75,000 broker bond pay anything to crash victims?

No. The $75,000 surety bond under 49 CFR § 387.307 protects motor carriers from unpaid freight charges and shippers from cargo losses. It does not cover bodily injury or wrongful death claims. A personal injury claim against a freight broker cannot be satisfied from the bond; it requires either the broker’s voluntary contingent liability insurance or a judgment against the broker’s own assets.

What is the difference between a freight broker and a motor carrier?

A freight broker arranges transportation but does not operate trucks or employ drivers. A motor carrier owns or leases the equipment and employs or contracts the driver. In a crash, the motor carrier faces primary liability for the driver’s negligence. The freight broker faces potential liability only for its own conduct, specifically, its selection of that carrier. The broker’s liability theory is negligent selection, not respondeat superior, which is why the broker can be a viable defendant even when the motor carrier’s coverage is in place.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...