Reservation of Rights Letters in Texas Injury Claims

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- A reservation of rights letter is not a denial; your injury claim stays active during the investigation.

- Texas Insurance Code § 542.056 gives insurers 15 business days to accept, reject, or reserve rights.

- Never give a recorded statement after an ROR letter without first speaking to an injury attorney.

You were rear-ended on I-35 outside Round Rock, and your back has been hurting since the day of the crash. Now a letter has arrived from the other driver’s insurance company. It says the company is “reserving its rights” while it investigates, and the legal language reads like a warning shot you don’t quite know how to answer.

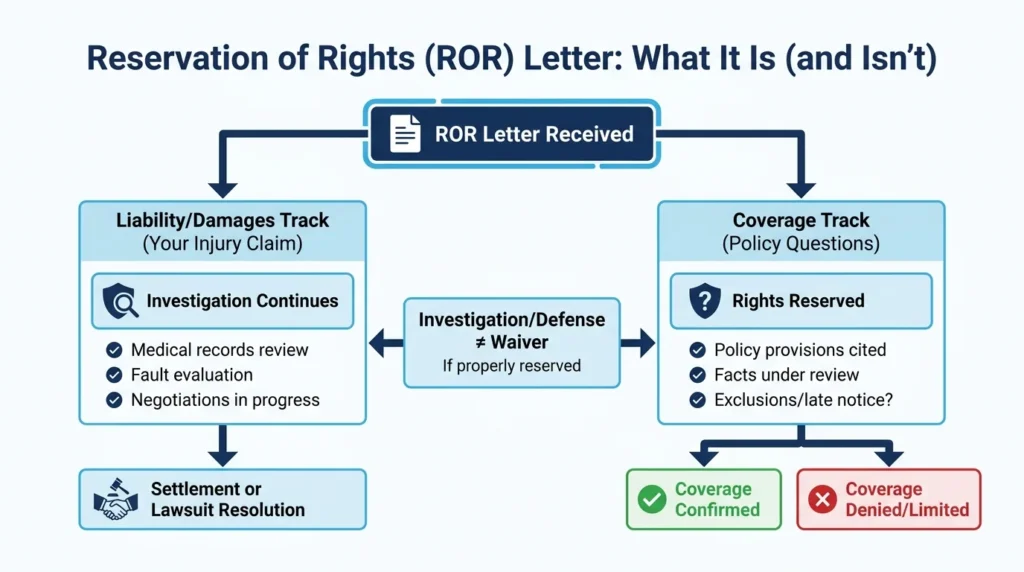

What Is a Reservation of Rights Letter?

A reservation of rights (ROR) letter is a formal written notice that the insurer is continuing to investigate the claim while keeping its right to dispute or deny coverage later. It is not a coverage acceptance, nor is it a denial. The letter holds both outcomes open, which is why it confuses so many claimants.

Insurers send these letters when a coverage question exists alongside a liability question. The two issues run on parallel tracks. The letter keeps the insurer’s legal options intact on the coverage track while the claim itself stays active.

A typical ROR letter identifies the specific policy provisions or exclusions the insurer is investigating, and it states the facts under review. It also declares that any defense or investigation work the insurer performs does not waive its right to later contest coverage. What the letter includes, and what it leaves out, sets the boundaries of what the insurer can argue later.

Why Texas Insurers Send ROR Letters

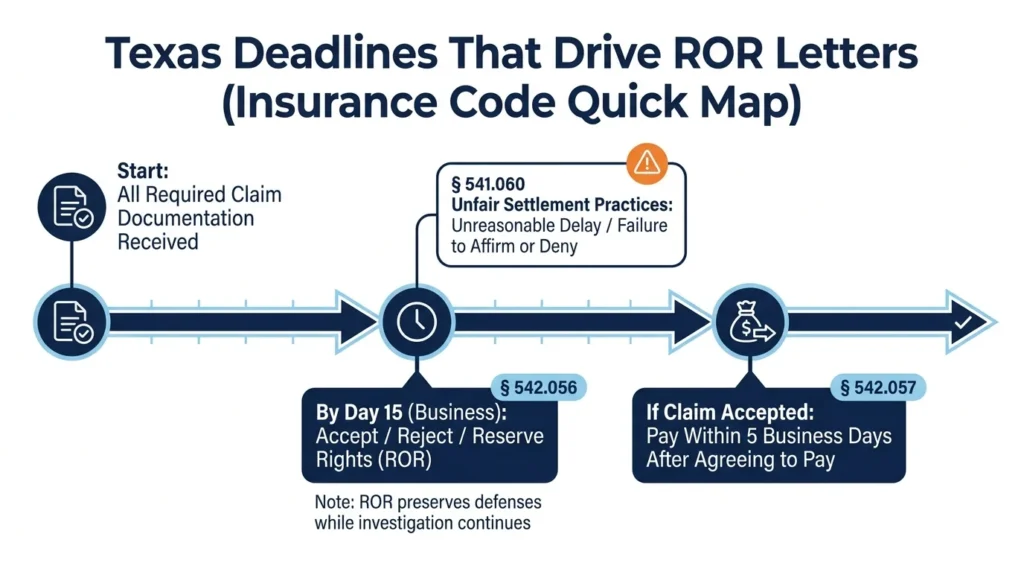

Texas law forces insurers to act on claims quickly, and the ROR letter is one of the tools they use to meet that obligation without committing to coverage. Two sections of the Texas Insurance Code drive this behavior. Together, they create both a deadline and a penalty for missing it.

- Under Texas Insurance Code § 542.056, an insurer must notify a claimant of acceptance or rejection of a claim no later than the 15th business day after receiving all required documentation. An ROR letter is one way insurers meet that deadline while the coverage investigation stays open.

- A second statute adds teeth. Texas Insurance Code § 541.060 prohibits unfair settlement practices, including, as Texas courts and regulators have interpreted it, as failing to affirm or deny coverage within a reasonable time. An insurer that neither accepts coverage, denies it, nor issues a timely ROR letter may risk waiving specific coverage defenses it failed to preserve a significant exposure that experienced coverage counsel can identify and exploit.

The practical driver is simple: when a claim raises a coverage question, such as a policy exclusion, late reporting, or a question about whether the insured’s conduct falls within the policy, the insurer cannot just sit on it. The ROR letter preserves the coverage defense while the insurer continues to investigate. You can read more about how Texas insurance claim investigations typically unfold and what insurers look for during that window.

How an ROR Letter Affects Your Injury Claim

An ROR letter changes the shape of your claim in three concrete ways:

- It signals that a coverage fight is possible.

- It creates protective doctrines you can use if the insurer overreaches.

- It operates differently depending on whose policy is at issue.

Understanding those three effects is what separates a claimant who panics from one who responds strategically.

First-Party vs. Third-Party ROR Letters

The letter affects you very differently depending on which insurer sent it.

A first-party ROR letter comes from your own insurer, often on an uninsured (UM) or underinsured motorist (UIM) claim, where you are both the insured and the claimant. Your own company is reserving its right to contest coverage on its own policy. Our guide to UM/UIM claims in Texas walks through how these disputes often unfold.

A third-party ROR letter comes from the at-fault driver’s insurer, meaning you have no direct contract with that insurer, and its duty to defend runs only to its own policyholder. That limits your direct leverage on the coverage question, but the letter also signals a possible conflict between the insurer’s defense of its policyholder and the insurer’s interest in denying coverage. That conflict is where an experienced attorney can find strategic footing.

Insurer Waiver & Estoppel Risk

Two doctrines protect you when an insurer acts inconsistently with the position it took in the ROR letter.

- Waiver applies when an insurer defends or investigates in a way that contradicts a coverage defense it later tries to assert. Texas courts may find the insurer gave up that defense by its own conduct.

- Estoppel applies when you rely on the insurer’s behavior to your detriment, for example, by allowing the insurer to control a defense without independent counsel. The insurer may be blocked from raising coverage defenses it did not clearly preserve in the letter.

Texas courts read ROR letters strictly against the insurer. A letter that is vague, untimely, or fails to identify specific coverage defenses provides weaker protection to the insurer and stronger ground for you. A close read of the letter, alongside an understanding of how car accident claims work in Texas, often reveals where the insurer’s coverage position is weakest.

The Conflict of Interest an ROR Letter Can Create

When an insurer issues an ROR letter, it usually keeps providing defense counsel to its policyholder. That attorney technically represents the policyholder but is paid by the insurer, reserving the right to deny coverage. The loyalties can pull in opposite directions.

Here is the conflict in plain terms. The defense lawyer’s strategy may quietly favor the insurer’s coverage position at the cost of the policyholder’s liability defense. The lawyer might avoid arguments that would establish liability but undermine the coverage defense the insurer is trying to keep alive.

Texas law recognizes this problem, meaning when the coverage defense and the liability defense create genuinely adverse interests, the policyholder may have a right to independent counsel, sometimes called Cumis counsel, paid by the insurer. For you, as the injured claimant, this dynamic affects the consistency of the defense opposing your claim. It is especially common in commercial truck accident cases where multiple endorsements, exclusions, and driver-specific terms create overlapping coverage questions.

An attorney who handles insurance disputes can spot whether the ROR-driven conflict has shaped the opposing defense in ways that may actually benefit your claim.

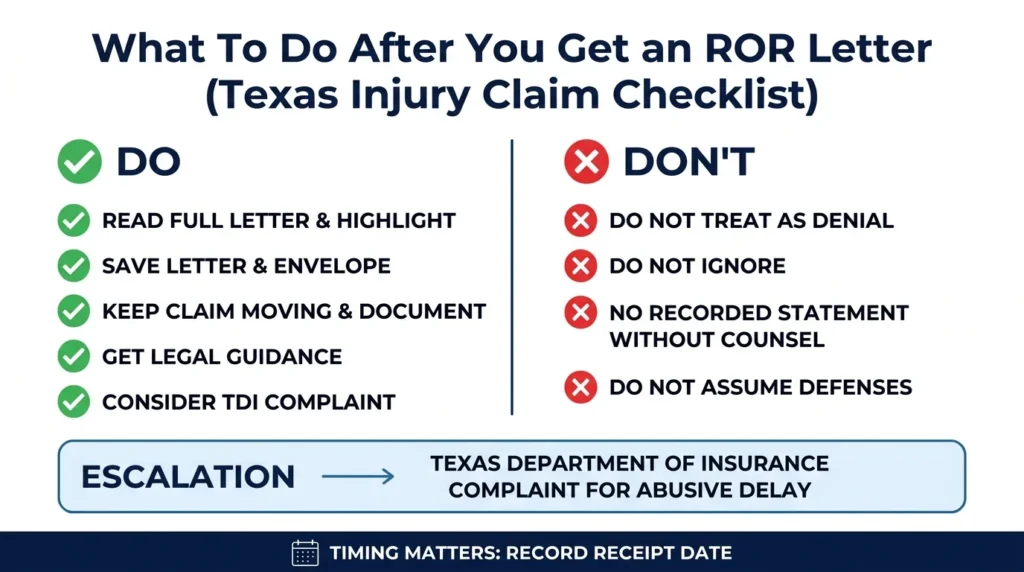

Steps to Take After Receiving an ROR Letter

Your response in the first days after the letter arrives can shape the rest of the claim. The goal is to protect your position without giving the insurer ammunition.

- Read the letter fully and identify the specific provisions cited. The coverage defense is bounded by what the insurer lists. Anything left out may be waived later.

- Do not treat it as a denial, and do not ignore it. Your claim is still active, and the investigation is open.

- Do not give a recorded statement without legal guidance. An ROR letter signals that the insurer is actively looking for grounds to limit or deny coverage, which raises the risk of a recorded statement.

- Save the original letter and note the date you received it. The timing matters if a bad-faith or estoppel argument comes up later.

If you believe the insurer is using the ROR process to delay payment or avoid a decision, the Texas Department of Insurance accepts consumer complaints about auto insurance conduct. Filing a complaint creates a record and sometimes prompts a faster response.

For a step-by-step on the claim itself, see our guide on how to file a car insurance claim in Texas. And if your claim involves serious injuries from a crash, our car accident practice explains how attorneys handle the insurance side of these cases.

Talk to a Texas Injury Attorney About Your ROR Letter

A reservation of rights letter is the moment when legal guidance matters most, because the insurer’s coverage position is still forming and the window to influence it is open. Angel Reyes & Associates has over 30 years of experience handling insurance-involved injury claims across Texas, with more than $1 billion recovered for clients.

We have a team of more than 600 dedicated professionals available 24/7 who are fluent in both English and Spanish. We offer free consultations; work on contingency, meaning you do not pay a fee unless we win; serve the entire state of Texas across more than 20 offices statewide; and can handle most of your case remotely. Look through our past case results or meet the attorneys on our team, then contact us today to talk through your letter.

Past results do not guarantee future outcomes.

Reservation of Rights (ROR) Letters FAQs

Can a third-party insurer settle my injury claim while coverage is still under an ROR?

Yes, an insurer can negotiate and settle a third-party claim even while an ROR is in place. The ROR letter addresses the coverage question between the insurer and its own policyholder, and settling your damages does not automatically resolve that separate dispute.

Does Texas law require an ROR letter to be sent in a specific way, such as certified mail?

Texas Insurance Code § 542.056 requires the notice to be mailed to the claimant’s last known address, but it does not mandate certified mail for every type of claim. Keeping your own dated record of when the letter arrived helps if a timing dispute comes up later.

If the at-fault driver's insurer denies coverage after sending an ROR letter, can I still sue the at-fault driver directly?

Yes, a coverage denial by the insurer does not eliminate the at-fault driver’s personal liability for your injuries. You can pursue a lawsuit against the driver directly, though collecting a judgment depends on whether the driver has personal assets.

How long does a Texas insurer have to finish its coverage investigation after sending an ROR letter?

Texas law does not set a fixed deadline for completing a coverage investigation, but Texas Insurance Code § 542.057 requires payment of accepted claims within five business days of agreeing to pay. Unreasonable delays in completing the investigation can support a bad-faith complaint.

Can an insurer issue more than one ROR letter on the same claim?

An insurer can send a supplemental ROR letter if new facts surface during the investigation that raise additional coverage questions. Each letter should identify the new grounds being reserved, and Texas courts will still construe any vague or missing language against the insurer.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...