A Texas Uninsured Motorist Accident Guide

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Between 14-20% of Texas drivers are uninsured, and even more don't have enough coverage for a serious wreck.

- UM coverage pays for injuries and damage when an at-fault driver has no insurance or flees the scene.

- Late notice, disputed liability, and treatment gaps are the top reasons insurers deny UM claims.

What Happens If You’re Hit by an Uninsured or Underinsured Driver in Texas?

You’re heading north on US-75 toward Plano when a driver drifts across two lanes and clips your bumper near the Park Lane exit. They pull over, hand you a license, and admit they let their policy lapse three months ago.

Now, you’re standing on the shoulder of the road with a damaged car, a sore neck, and an at-fault driver who has no insurance to pay for it. What happens next depends almost entirely on coverage you may not even know you have.

What Is Uninsured Motorist Coverage?

Uninsured motorist (UM) coverage is an add-on to your own auto policy that pays for injuries, and, in some cases, property damage caused by a driver who has no insurance. It helps pay when the at-fault driver’s insurance would normally cover the damage.

UM policies also cover hit-and-run crashes and certain phantom-vehicle scenarios (for example, if someone cuts you off or forces you to swerve and crash, then drives away).

Texas does not require you to carry UM coverage, but insurers must offer it to every applicant. Under the Texas Insurance Code (TIC) SS 1952.101, UM coverage must be included unless you reject it in writing. If there is no signed waiver rejecting the coverage, then your policy may include UM benefits even if you thought it didn’t.

UM coverage is split into two parts. Uninsured motorist bodily injury (UMBI) pays for medical bills, lost wages, and pain and suffering. Uninsured motorist property damage (UMPD) pays for vehicle repairs, usually with a $250 deductible. Both apply when the other driver has no insurance at all.

UM also covers hit-and-run crashes in which the driver who is responsible flees the scene. These cases require careful documentation, and the rules are different from a standard claim. Our guide on hit-and-run accidents in Texas explains the evidence that carriers require. The Texas Department of Insurance consumer bulletin is a useful starting point for understanding how the coverage actually works.

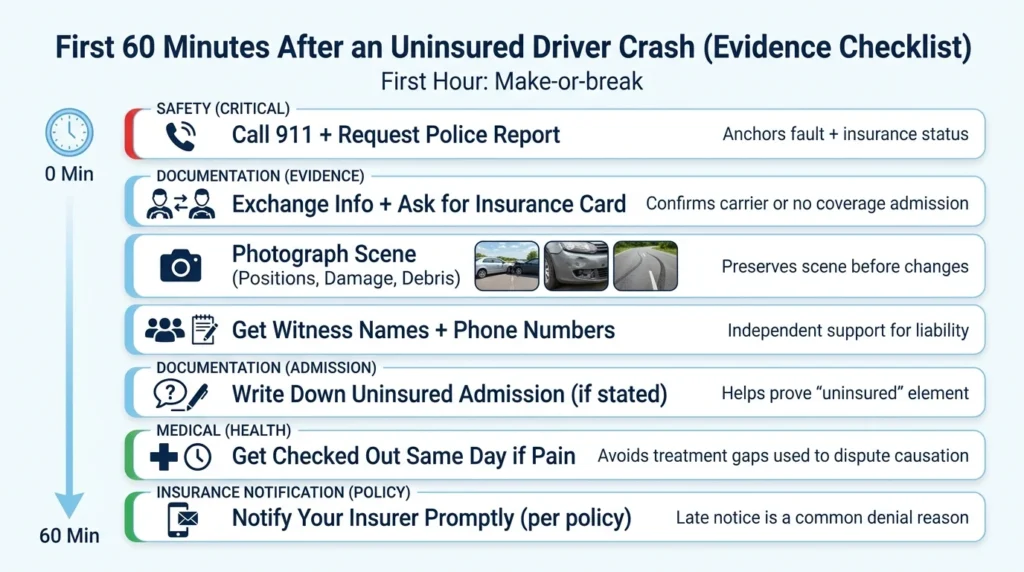

Take These Steps After an Uninsured Driver Accident

After a crash with an uninsured driver, the first hour is make-or-break. Call 911, get a police report, and exchange any information you can collect. Photograph the scene, the vehicles, and any visible injuries. Get names and phone numbers from witnesses before they leave. These steps will ensure that you have the evidence your insurer will need later.

If possible, confirm the other driver’s insurance status. Ask for their insurance card and write down the carrier name and policy number. If they admit they have no coverage, write it down. Officers often verify insurance through the state database, and the police report will reflect what they find. This report will be the backbone of your UM claim.

Document everything before you leave the scene. Take wide shots of vehicle positions, close-ups of damage, and pictures of skid marks or debris.

If you feel any pain, get checked out the same day. Gaps in medical treatment give insurance adjusters a reason to argue your injuries came from somewhere else.

Our checklist on what to do after a Texas car accident includes all the steps in order.

Be sure to notify your own insurance company within the timeframe required by your policy (often within a few days). Tell them the other driver was uninsured, and you intend to open a UM claim. An attorney can help you navigate these early conversations, so you don’t say anything that could reduce how much money you get later.

Filing Your Uninsured Motorist Claim

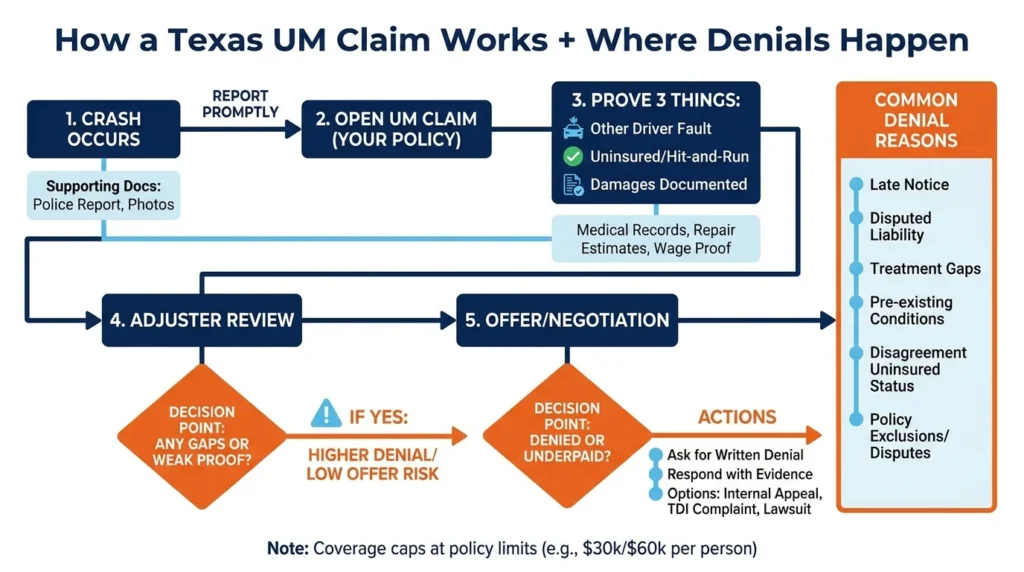

A UM claim is a claim against your own insurer, but it works like a third-party liability claim. You must prove the other driver was at fault, that they lacked insurance, and that your damages are real and documented. Your carrier will assign an adjuster to your case, request records, and eventually make an offer. It is your responsibility to prove your case.

Gather your evidence early. You will need the police report, photos, medical records, repair estimates, and proof of lost income. If the at-fault driver was uninsured, your insurer may want confirmation from the state’s verification system, or a denial letter from the other carrier. Keep copies of everything you send out.

Texas does not set a single legal deadline for UM claims, but your insurance policy does. Most policies require you to report the crash promptly and file a formal claim within two years, similar to personal injury lawsuit deadlines. If you miss the policy deadline, the carrier can refuse to pay. Read your policy papers or call your agent if you are unsure.

UM coverage also interacts with other parts of your policy. Personal injury protection (PIP) and medical payments (MedPay) typically pay first for medical bills, regardless of fault. Collision coverage can repair your vehicle while the UM claim is pending.

If the at-fault driver has some insurance but not enough, underinsured motorist (UIM) benefits may cover the difference. Our breakdown of underinsured motorist coverage in Texas explains how these layers of coverage fit together.

Settlement negotiations with your own insurer can feel like a fight because it often is one. According to the Insurance Information Institute, Texas has approximately 14% uninsured drivers, which is close to the national average. This means UM claims are common, and carriers handle them aggressively. Your insurer’s job is to pay as little money as possible to close out the claim.

Common Claim Denials and Appeals

Insurers deny UM claims for a handful of recurring reasons. The most common are late notice, disputed liability, gaps in medical treatment, pre-existing conditions, and disagreement over whether the other driver was actually uninsured. Some denials are legitimate, but many are just tactics to try to get a better deal.

Coverage disputes often depend on the exact wording in your insurance policy. An adjuster may argue that your UM limits do not apply to a particular vehicle, or that an exclusion about household members invalidates your claim. Sometimes, these arguments are wrong. Texas courts have rejected some of them over the years. Our overview of Texas car insurance requirements covers the basics of what your policy must include.

If your claim is denied, ask for the denial in writing, pointing to the specific rule in your policy. Then respond in writing with the evidence and legal information explaining why you disagree. At this stage, many denials get reversed, but if yours doesn’t, then you can file a complaint with the Texas Department of Insurance, ask for an appeal process if your policy allows it, or file a lawsuit for breach of contract and bad faith.

The amount of money you can get depends on your coverage limits. UM benefits only pay up to the limit listed in your policy (often $30,000 or $60,000 per person). If your damages are higher than your limit, then the carrier only has to pay you the policy’s maximum, and not a dollar more. This is when an attorney becomes critical, because you may need to identify other ways to recover money.

Work With Angel Reyes & Associates

If an uninsured driver hit you in Texas, you do not have to fight your own insurance company alone. Angel Reyes & Associates has more than 30 years of experience handling car accident claims and has recovered more than $1 billion for clients across the state. We work on a contingency basis, meaning you pay no fee unless we win, and consultations are free.

Contact us any time, day or night, and review our case results or our dedicated uninsured and underinsured motorist practice to see how we approach these claims.

Past results do not guarantee future outcomes.

Uninsured Motorist FAQs

What happens if the uninsured driver who hit me has assets that I can pursue?

You can sue an uninsured driver directly and try to collect from their personal assets (such as bank accounts or property). However, most uninsured drivers lack significant assets, which makes your UM coverage a more reliable source of recovery.

Can I stack multiple uninsured motorist policies if I own several vehicles?

Texas follows modified comparative negligence rules, so you can still recover UM benefits even if you were partially at fault. Your recovery will be reduced by your percentage of fault, as long as you are less than 51% responsible.

Does uninsured motorist coverage apply if I am a passenger in someone else's car?

Yes, your UM coverage typically applies if you were a passenger in another vehicle. You may also be covered under the vehicle owner’s UM policy, which potentially gives you multiple sources of coverage.

How long does it typically take to settle an uninsured motorist claim in Texas?

Simple UM claims with clear liability and minor injuries often settle within 3-6 months. Complex cases involving serious injuries or disputed fault can take 12-18 months or longer to resolve.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...