How Cargo Insurance & Securement Rules Affect Texas Truck Accident Claims

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Cargo-related truck accidents often involve multiple liable parties, each potentially carrying separate insurance policies.

- Federal cargo securement rules under 49 CFR § 393.100 establish safety standards, and violations can serve as evidence of negligence.

- Texas's 51% bar rule means identifying all responsible parties can protect your recovery by ensuring that fault is properly allocated among all defendants.

You were driving on I-35E near Lower Greenville when a flatbed ahead of you lost part of its load. Steel pipes scattered across the highway. You swerved, but one struck your windshield.

Now, you’re dealing with injuries, a totaled car, and an insurance adjuster who keeps asking questions about “the shipper” and “the loading crew.” You’re not sure who’s responsible, or how many insurance policies might apply to your situation.

Cargo-related truck accidents in Texas often involve more parties, insurance policies, and finger-pointing than a typical collision. Understanding how cargo insurance intersects with your bodily injury and property damage claim can help you protect your rights and pursue fair compensation.

Why Cargo Issues Are Important For Your Texas Truck Accident Claim

When cargo shifts, spills, or falls from a commercial truck, the crash investigation expands beyond the driver. In this case, three separate concerns often overlap:

- Injury and property damage to the public (your claim)

- Damage or loss to the cargo itself (the shipper’s concern)

- Cargo-related negligence that caused the crash (the liability question)

Your claim focuses on the first category. However, the facts surrounding the second and third categories can significantly affect who you can hold responsible and how much insurance coverage may be available.

A shifting cargo truck accident often creates additional defendants. The driver, the trucking company, the company that loaded the freight, and even the shipper or broker may share responsibility. Each of these parties may carry separate insurance policies. This means more potential sources of compensation for your injuries and vehicle damage.

Cargo insurance itself typically protects cargo owners against lost or damaged goods during transit. It usually does not pay injury victims directly. However, cargo-related facts can still increase your claim’s value by establishing clear negligence and expanding the number of responsible parties available.

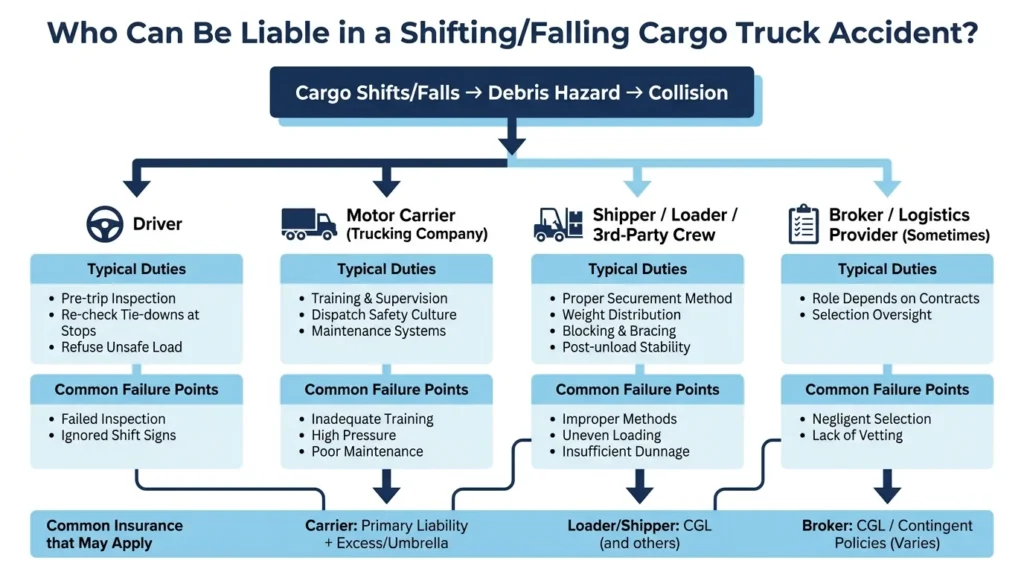

Who May Be Liable When Cargo Shifts or Falls in Texas

Texas cargo cases frequently involve multiple defendants. The central question is: who had control over loading, securing, inspecting, and transporting the freight?

Evidence often points to more than one party. A driver may have failed to inspect tie-downs. A loading crew may have used insufficient straps. A trucking company may have pressured the driver to skip safety checks. Under Texas proportionate responsibility rules, fault can be divided among all responsible parties.

Common scenarios include lumber or pipe spills on highways like US-75, improperly palletized freight shifting on the DNT, and construction materials falling from trucks traveling through Plano or Garland.

The Truck Driver & Motor Carrier

Most cargo accident claims start with the driver and the trucking company. The carrier typically provides the primary liability insurance policy and controls driver training, dispatch decisions, and safety compliance.

Drivers have specific duties related to cargo, including:

- Conducting pre-trip inspections of load securement

- Checking tie-downs during transit stops

- Refusing to transport unsafe loads

- Adjusting speed for high center-of-gravity loads

When drivers do not complete these duties, the trucking company may also bear responsibility through its policies, supervision practices, and safety management systems. The carrier’s commercial truck insurance is often the first layer pursued for injury and property damage claims.

Shippers, Loaders, & Third-Party Loading Crews

When someone other than the driver loaded or secured the freight, liability can expand to include other parties. Common loader mistakes include:

- Using improper tie-down points

- Providing insufficient securement for the cargo type

- Creating uneven weight distribution

- Failing to use adequate blocking, bracing, or dunnage

Loading and unloading creates specific risks. A partial unload at a stop in Frisco or Addison can leave remaining cargo unstable. Broken straps or forklift damage to pallets may go unnoticed until the load shifts on the highway.

These entities often carry their own commercial general liability (CGL) policies. Adding them as defendants can increase the total insurance coverage available for your claim.

Brokers & Logistics Providers

Freight brokers arrange transportation but typically do not own trucks or employ drivers. Their role in the liability depends on their specific conduct and contractual relationships.

In this case, it’s helpful to understand the shipping chain. The bill of lading, shipping labels, DOT number, and MC number on the truck can help identify all parties involved. Documenting this information at the scene (when it is safe to do so) can help your attorney trace responsibility and locate applicable insurance policies. Our guide on what to do after a truck accident covers evidence collection in detail.

Federal Cargo Securement Rules & Texas Liability

The Federal Motor Carrier Safety Administration (FMCSA) establishes cargo securement rules that apply to most commercial trucks. These regulations require cargo to be firmly immobilized or secured to prevent shifting or falling during normal driving conditions.

The general requirements appear in 49 CFR § 393.100. This regulation specifies that cargo must be contained, immobilized, or secured to prevent it from shifting, falling, or otherwise becoming a hazard during transportation.

Violations of these federal standards can serve as powerful evidence of negligence. Inspection reports, citations, strap or tie-down failure analysis, and expert reconstruction can all demonstrate that a party failed to meet the required safety standards.

How Shifting Cargo Causes Crashes

When cargo shifts inside or on top of a trailer, it changes the truck’s center of gravity. This can cause:

- Loss of vehicle control during lane changes or braking

- Rollover accidents

- Jackknife incidents

- Debris striking vehicles behind the truck

Defendants often blame each other. A carrier may claim that the shipper loaded the freight improperly. The loader may argue that the driver failed to inspect or retighten securement devices during transit.

If you’re involved in a cargo-related crash, try to safely document the debris field, any visible straps or chains, the trailer’s condition, and company markings on the truck. Witness contact information is also valuable.

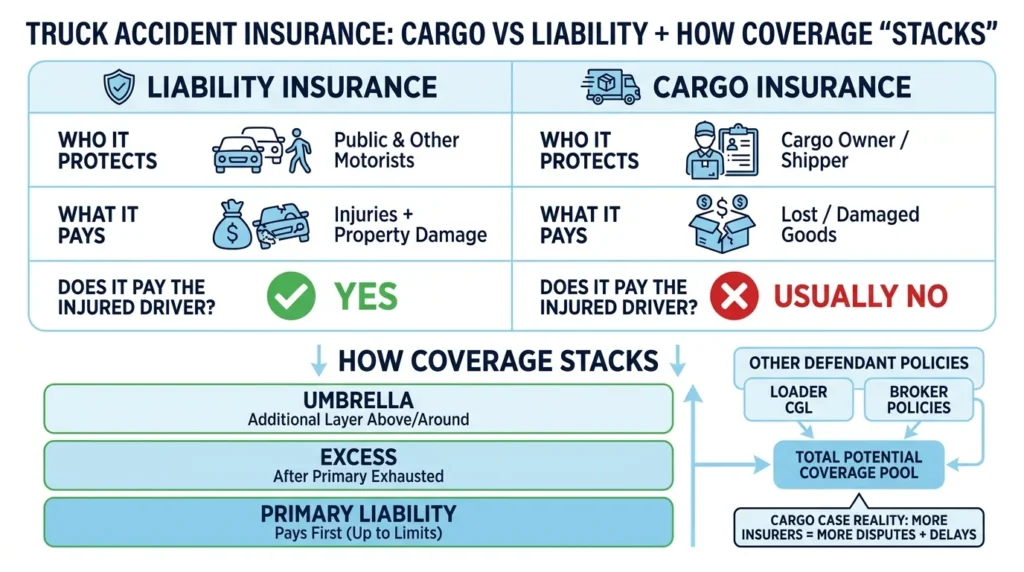

Cargo Insurance vs Liability Insurance

Many accident victims confuse these two types of coverage. Understanding the difference helps set realistic expectations.

Liability insurance covers injury and property damage to others. This is what pays your medical bills, lost wages, and vehicle repairs.

Cargo insurance covers loss or damage to the goods that were being transported. This protects the shipper or cargo owner, not the crash victims.

The FMCSA’s insurance filing requirements show when cargo insurance is required. Notably, carriers of household goods must carry cargo insurance, but many other carrier types are not subject to this requirement.

Texas Transportation Code Chapter 643 addresses motor carrier registration and includes provisions for liability and cargo insurance for certain carriers operating in Texas.

Even when cargo insurance isn’t mandatory for a particular carrier, other policies (such as liability, excess, or umbrella) may still apply to your damages. The specific details about the cargo can strengthen your claim by establishing clear negligence and identifying additional responsible parties.

How Insurance Coverage Stacks in Truck Accident Cases

Commercial trucking operations often carry multiple layers of insurance, including:

- Primary liability coverage (the first policy to pay)

- Excess coverage (which kicks in after primary limits are exhausted)

- Umbrella policies (which provides additional protection for other layers)

When cargo-related defendants enter the picture, each may carry separate policies. The trucking company, shipper, loading company, and broker might all have their own coverage. This can create multiple potential sources of compensation.

However, multiple insurers also means more complexity. Trucking companies and insurers often use delay and denial tactics to minimize payouts. Each insurer may point fingers at other parties, hoping to shift responsibility elsewhere.

Identifying Coverage Early

Collecting certain information at the scene can help your attorney locate all applicable policies. This information includes:

- DOT and MC numbers from the truck

- Trailer numbers and company names on the cab

- Shipper and receiver information from any visible paperwork

- Photos of debris, damaged tie-downs, and the load type

Avoid giving recorded statements to insurance adjusters before consulting an attorney. Don’t assume that one insurer represents the only available coverage.

Texas’s 51% Bar Rule & Proportionate Responsibility

Texas follows a modified comparative fault system under Texas Civil Practice and Remedies Code Chapter 33. Two key rules apply:

- Your recovery is reduced by your percentage of fault. If you’re found 20% responsible, your compensation is reduced by 20%.

- You cannot recover anything if you’re more than 50% at fault. This is known as the “51% bar.”

In cargo cases, defendants often argue that the victim should have avoided the debris, they were following too closely, or they made an unsafe maneuver. Strong evidence of securement violations and clear causation can help counter these arguments.

Why Multiple Defendants Make a Difference in Fault Allocation

Identifying all responsible parties isn’t just about finding more insurance. It also affects how fault is divided.

If the driver, carrier, and loading company all share responsibility, the fault attributed to you may decrease. This can prevent the 51% bar from blocking your recovery entirely and lessen the risk of any comparative fault reduction to your damages.

You should only pursue parties that are supported by actual evidence, documents, and securement standards. Experienced truck accident attorneys know how to build these cases properly.

What to Do After a Cargo-Related Truck Accident

If you’re involved in a crash caused by shifting or falling cargo anywhere in Texas:

- Call 911 and report the debris hazard to protect other drivers.

- Get medical evaluation even if your injuries seem minor.

- Don’t move evidence unless it is necessary for safety.

- Document everything safely including cargo type, securement devices, company markings, and debris location.

- Collect witness information.

- Be cautious with insurance adjusters and avoid making recorded statements before consulting an attorney.

- Keep records of your symptoms, missed work, and repair estimates.

How Angel Reyes & Associates Can Help

Cargo-related truck accidents involve rapidly shifting evidence. Cleanup crews will quickly remove debris. Tow trucks will haul away damaged vehicles. Freight will get reloaded and shipped. Acting quickly to preserve evidence is critical.

Angel Reyes & Associates has over 30 years of experience handling complex truck accident claims across Texas. We can identify all responsible parties, locate applicable insurance policies, and coordinate claims across multiple insurers and defense teams.

We offer free initial consultations and work on contingency. You pay no fee unless we win. We’re available 24/7 and serve clients throughout Texas from our more than 20 locations statewide. Se habla español.

If a cargo-related truck accident has left you with injuries and unanswered questions, contact us to discuss your situation, or read what past clients say about working with us.

Cargo Insurance FAQs

Can a truck broker be responsible for a cargo-related crash in Texas?

Sometimes, but not automatically. A broker is more likely to face claims if its own conduct played a role, such as providing unsafe instructions or hiring an unqualified or unsafe carrier, and the specific facts and contracts are what will determine liability.

What if the truck was carrying household goods when the crash happened?

Household-goods carriers are more likely to be subject to cargo insurance requirements under federal and Texas rules. This does not mean cargo coverage will pay an injured driver directly, but it can be relevant when sorting out all available policies.

Does a police report usually list the shipper or loading company?

Not always. Police reports often identify the driver, the carrier, and basic facts about the crash, but shipping paperwork, bills of lading, trailer markings, and business records may be required to find the shipper or loading company.

Can a cargo claim and an injury claim be handled at the same time?

Yes, they are often handled simultaneously because one claim may involve damage to the freight, while another may involve injuries and vehicle damage. These parallel claims can affect negotiations because insurers may dispute when and how the load problem happened.

What happens if the cargo was loaded correctly but shifted after hard braking or a sudden maneuver?

This can still lead to a dispute over whether the securement was adequate, the driver responded reasonably, or both. In many cases, the answer depends on the load type, the securement method, and what the evidence shows about the truck’s movement right before the crash.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...