Commercial vs Personal Auto Insurance in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Personal auto policies in Texas carry $30,000/$60,000/$25,000 minimums. Under federal law, commercial truck companies must have at least $750,000 in liability coverage.

- Most personal auto policies exclude coverage when the vehicle is used for commercial purposes, such as deliveries or rideshare driving.

- If a working driver's personal insurer denies a claim, the employer's commercial policy or the employer directly may be the right target.

You’re out doing errands when you get hit by a driver in an unmarked sedan. After recovering from the initial shock, you get the individual’s insurance information and assume that your claim will go through their personal policy. But a few days later comes another unpleasant surprise: The insurer calls to say that coverage has been denied because the driver was making deliveries at the time, an activity that is excluded from coverage on a personal auto policy.

Now you’re in limbo as you wait with medical bills and car repair expenses. As the injured party, it is important that you learn the difference between commercial and personal auto insurance so you know who will cover your losses.

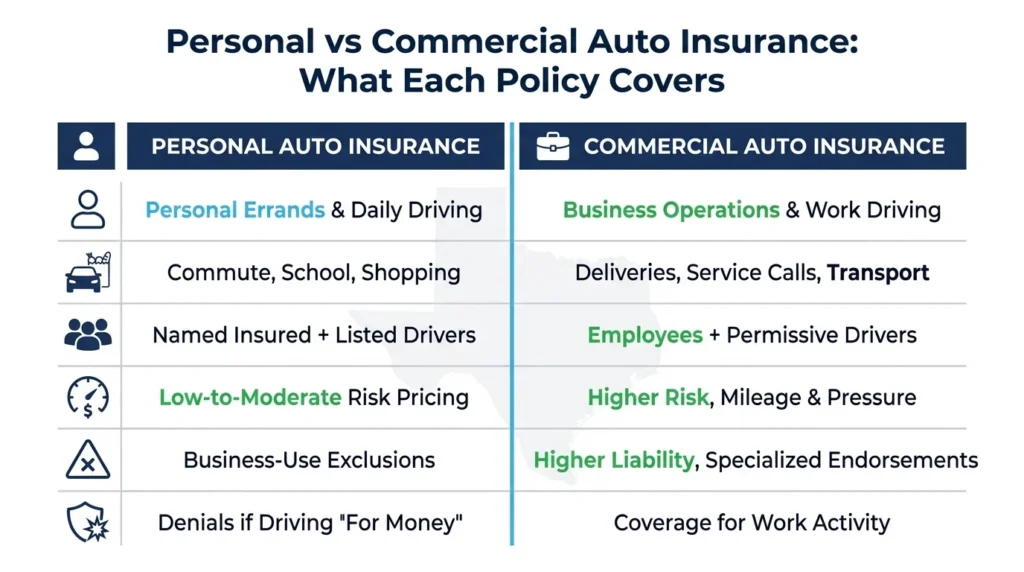

What Each Policy Is Designed to Cover

Personal auto insurance covers the named insured driving for personal, noncommercial purposes. Commercial auto insurance covers vehicles used for business, any licensed driver the employer lists on the policy, and the higher liability exposures that come with operating a working vehicle. The two policy types exist because the risks are fundamentally different.

Personal auto policies cover vehicles used for commuting to work and everyday driving. Commercial policies apply to vehicles that are used for business purposes. Most personal policies include a business-use exclusion. Our explainer of Texas commercial truck insurance requirements shows just how wide the gap in required coverage can be.

How Coverage Limits Compare

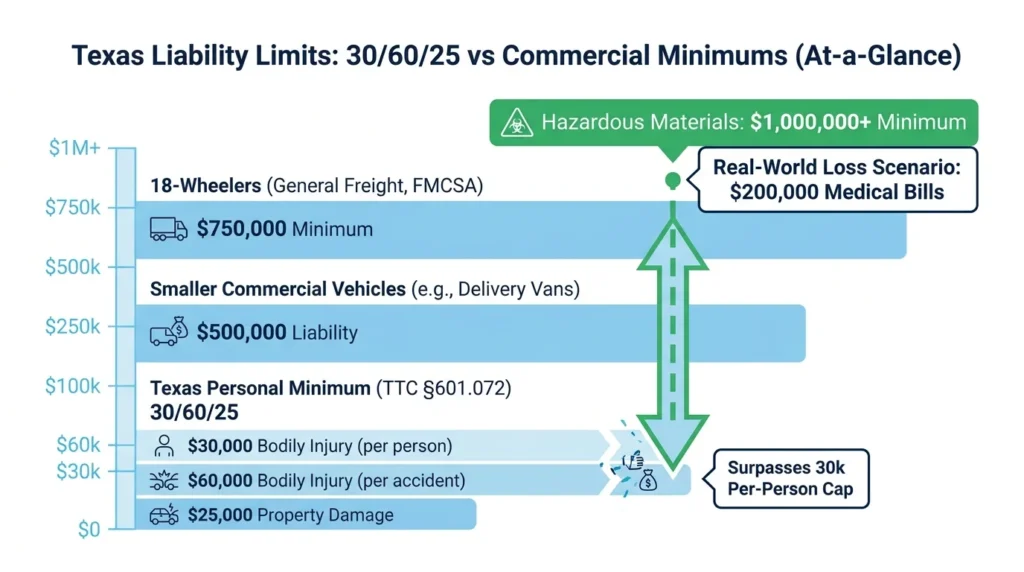

The most consequential difference between these two policy types is the money available to compensate you after a collision. Under Texas Transportation Code Chapter 601, § 601.072, drivers must carry minimum personal liability insurance of 30/60/25: $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. Those minimums are often not enough for a serious crash.

Minimum liability insurance for commercial trucking companies is much higher. Under Federal Motor Carrier Safety Administration rules (49 CFR, Part 387), most 18-wheelers transporting general freight must carry at least $750,000 in liability coverage. Carriers hauling hazardous materials have minimums of $1 million or more, though many voluntarily carry even higher levels.

Smaller commercial vehicles, such as vans and pickup trucks, often carry state-required minimum liability coverage of $500,000.

If you’re in a serious crash that results in, say, $200,000 in medical bills, this claim will exhaust a personal auto policy minimum almost immediately. A commercial policy, though, may cover the full loss.

The Business-Use Exclusion Problem

Most Texas personal auto policies explicitly exclude coverage when the vehicle is used to transport goods or people for money. That exclusion exists because the insurer priced the policy based on personal driving risk, not commercial risk. When a driver crosses into commercial territory, the insurer steps back.

Common scenarios that trigger this exclusion:

- Delivery drivers using personal vehicles without a commercial endorsement

- Rideshare drivers not disclosing their activity on the app

- Employees using personal cars to run work errands

If the driver who hit your car falls into one of the above categories, their insurer can deny the claim entirely based on the exclusion language in the policy. And that means you need to go after the employer’s commercial insurer or the employer directly, or seek compensation for your losses from your own uninsured/underinsured motorist coverage.

Rideshare platforms have created a partial exception. Both Uber and Lyft maintain commercial contingent coverage that activates once a driver accepts a trip request. But coverage varies based on what the driver’s status is in the app when the collision occurs. Before a driver accepts a request, only minimal contingent coverage applies. Once the trip is active, coverage typically reaches $1 million.

Which Policy Applies After a Crash?

The answer to that question depends on two things: who owns the vehicle and what the driver was doing at the time of the incident.

Start with the vehicle. A company-owned vehicle almost always triggers commercial coverage. A personally owned vehicle may trigger personal coverage, commercial coverage, or both, depending on what the driver was doing.

Identify the activity. A driver on a personal errand is typically covered by their personal auto insurance policy. A driver actively working, making a delivery, or responding to a dispatch call should have commercial coverage. When commercial coverage is missing and it should exist, the employer may face direct liability.

Get both pieces of information at the scene. Request the driver’s personal insurance card and ask whether they were working at the time. If they were, ask for the employer’s name and insurance information. Understanding how Texas insurers investigate car accidents can help you anticipate what questions will come next.

Work with an Experienced Attorney

Sorting out which insurance policy applies after a crash involving a working driver can be difficult, especially when a personal insurer denies the claim. Angel Reyes & Associates has handled Texas commercial and personal auto claims for over 30 years. Our case results demonstrate our attorneys’ dedication to our clients’ success. And we work on contingency, meaning we receive no fee unless we win your case. Contact us for a free consultation.

Past results do not guarantee future outcomes.

Commercial vs. Personal Auto Insurance FAQs

What is a commercial auto endorsement, and does it solve the exclusion problem?

Some personal auto insurers offer, for a higher premium, a business-use endorsement that extends coverage to occasional work driving. These endorsements, however, typically do not cover vehicles used full-time for business or for transporting cargo for hire. A standalone commercial policy is usually required for those situations.

Does commercial auto insurance cover employees who drive their own cars for work?

Not automatically. A commercial policy typically covers vehicles the business owns or leases. To cover employees driving personal vehicles on work tasks, a business needs a non-owned auto liability endorsement added to the commercial policy. Without it, the employer may still face liability but without an insurance policy to cover it.

How do I find out if a commercial vehicle has adequate insurance before my case settles?

Your attorney can request the declarations page of the commercial policy through discovery. For federally regulated motor carriers, insurance filings are also publicly available in the Federal Motor Carrier Safety Administration ‘s Safety and Fitness Electronic Records database. Reviewing these records before settling tells you whether a higher-limit policy exists.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...