How Long Insurers Have to Pay Claims Under Texas Law

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas insurers have 15 days to acknowledge a claim and 5 business days to pay once accepted.

- Missing a Chapter 542 deadline triggers 18% annual interest, plus mandatory attorney fees.

- Chapter 542A weather claims follow modified deadlines and a lower variable interest rate.

You filed your claim weeks ago after a wreck on I-35 near downtown Austin, and the adjuster keeps asking for one more document. The check still hasn’t arrived, and bills are stacking up on your kitchen counter. You’re starting to wonder if the delay is normal, or if your insurer is breaking the law.

How the Texas Prompt Payment Law Works for Insurance Claims

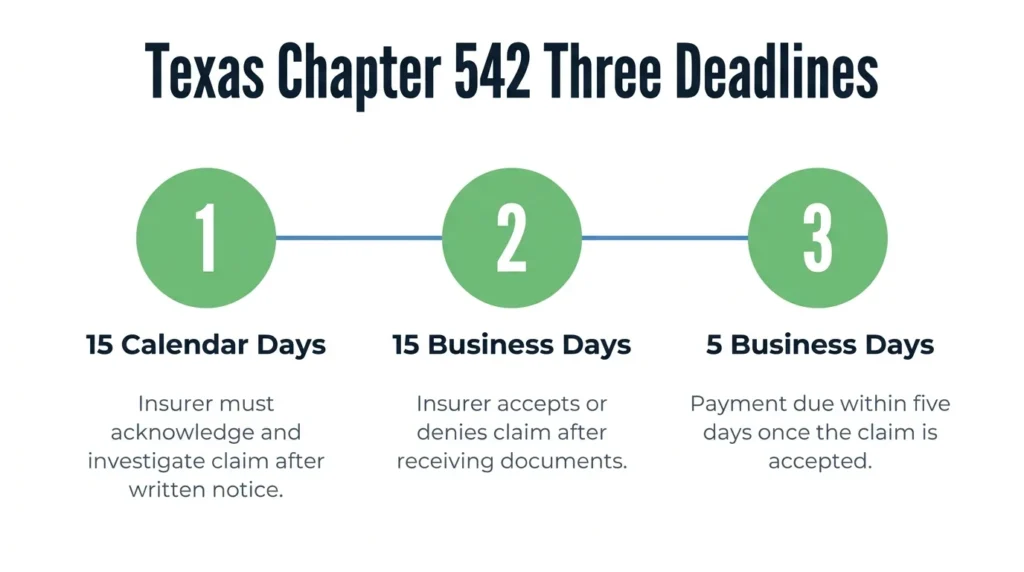

Texas law gives insurers three hard deadlines to handle a claim:

- 15 calendar days to acknowledge it

- 15 business days to accept or deny it after getting all requested documents

- 5 business days to pay once they accept it

The following rules come from the Texas Insurance Code Chapter 542, also known as the Prompt Payment of Claims Act:

- Stage 1 starts the moment the insurer receives written notice of your claim. Under Section 542.055, the company must acknowledge the claim, begin investigating, and request any extra items it needs within 15 calendar days.

- Stage 2 begins only after you’ve turned over every document the insurer asked for. Section 542.056 then gives the insurer 15 business days to accept or deny the claim. The insurer can extend this in writing, but they must accept or reject the claim within 45 days of sending the extension notice to the claimant.

- Stage 3 is the payout window. Once the insurer notifies you that they accept all or part of the claim, Section 542.057 requires payment within 5 business days.

When the Clock Starts for Each Deadline

Each stage has its own trigger:

- Stage 1 starts upon written notice.

- Stage 2 starts when the insurer has every requested document in hand.

- Stage 3 starts when the insurer issues its acceptance notice, not when you receive the check.

Insurers often delay claims by quietly resetting these triggers, so it’s critical to keep track of the dates you submitted each item.

Verbal notice does not start Stage 1. Send a written notice and keep proof of delivery (such as certified mail, email, or a portal confirmation).

In Stage 2, every new request from the insurer can pause the clock until you respond. Track every back-and-forth with dates, so you know exactly when the 15 business days begin.

Section 542.058 addresses situations in which an insurer delays payment after receiving all requested items. Courts have examined whether certain delays excuse the insurer from penalties, but the specific grounds and burdens involved depend on the facts and applicable case law. Our overview of the Texas insurance investigation process explains how to tell legitimate document requests from delay tactics.

Keep a dated log of every communication. Note when the claim was filed, when each document went out, and when an acceptance or denial came back. This log will prove a missed deadline later.

What Is Legally Covered in Catastrophe Claims?

Not every claim follows the standard timeline. Chapter 542 only applies to first-party claims. Storm-related claims fall under a separate chapter, with different rules and a different penalty rate. Knowing which framework applies to your claim is the first step to take before you start counting down the days.

What Claims Are Exempt from Chapter 542?

Chapter 542 covers first-party claims, meaning claims against your own insurer. Third-party claims (such as a claim against the at-fault driver’s insurer) do not have the same deadlines or penalty interest.

Workers’ compensation, title insurance, marine insurance, and HMOs are also exempt. Surplus lines insurers usually aren’t covered by Chapter 542, either. The Texas Department of Insurance consumer guide on getting your claim paid is a useful reference if you’re unsure which category your policy falls into.

Weather-Related Claims

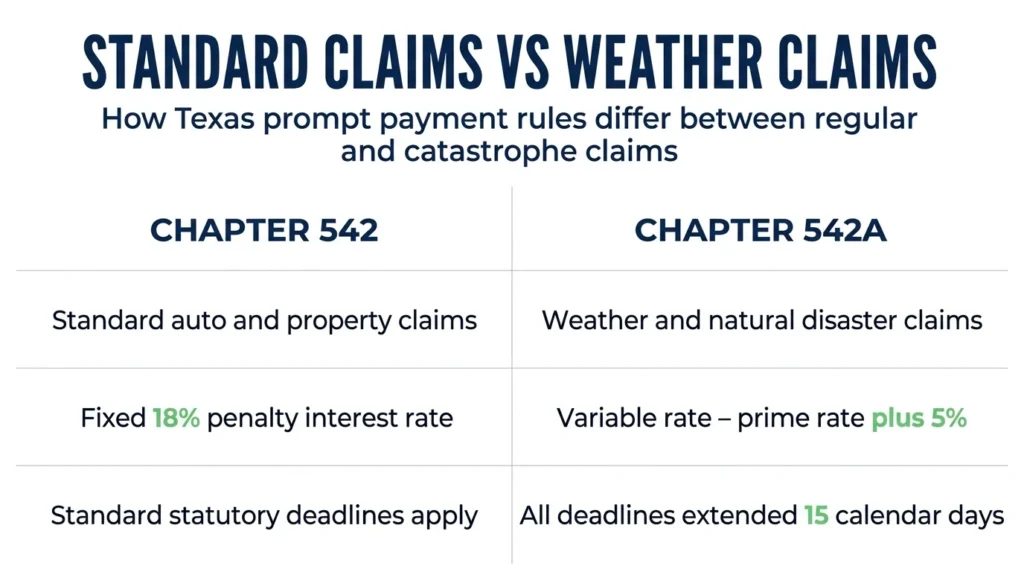

Texas Insurance Code Chapter 542A applies for claims tied to forces of nature, such as hail, hurricanes, floods, and other declared catastrophes. The timeline is similar but slightly different from regular insurance claims.

Under Section 542.059, when the commissioner designates a weather-related catastrophe or major natural disaster, all standard claim-handling deadlines are automatically extended by 15 additional calendar days.

Additionally, the penalty interest rate under Chapter 542A is not a fixed 18%. It is calculated by adding 5% to the post-judgment interest rate under Texas Finance Code Section 304.003. That rate fluctuates over time based on the prime rate and can range from 10% to 20% per year, depending on current rates. If your claim involves a storm or natural disaster, confirm which chapter applies before doing the math on what you may be owed.

If Insurers Miss the Deadline, What Happens?

Under Section 542.060, an insurer that misses the payment deadline owes the full claim amount plus 18% annual interest from the date the payment was due. Attorney fees are also mandatory, and you don’t have to prove bad faith to recover them. The missed deadline alone triggers the penalty.

Interest accrues on whatever remains unpaid. If the insurer cuts a partial check, then interest keeps building on the remaining amount. A partial payment doesn’t reset the clock or wipe out the penalty.

Chapter 541 of the Texas Insurance Code covers bad faith conduct separately, including misrepresentation, denial without reasonable investigation, and failure to attempt a fair settlement. A Chapter 542 violation can support a Chapter 541 bad faith claim, depending on the facts.

What to Do If Your Insurer Missed the Deadline

- Confirm the deadline was actually missed. Pull out the dated log and walk through each trigger point, including written notice, document submission, and acceptance notice. If the math shows a violation, then you have several options.

- File a complaint with the Texas Department of Insurance. TDI investigates insurer conduct and can push for compliance. Your complaint will also create an official record of the delay that can support a future claim.

- Consult an attorney before responding to any further insurer communication. Any statements you make after a violation can affect what damages you can recover.

Talk to an Attorney About Your Delayed Claim

A delayed claim isn’t just frustrating. Under Texas law, it’s a violation that comes with real consequences, including penalty interest and mandatory attorney fees. If your insurer misses a statutory deadline, it can give your claim more leverage.

Angel Reyes & Associates has more than 30 years of experience handling insurance delays and bad faith claims across Texas, with more than $1 billion recovered for clients. We work on contingency, meaning you pay no fee unless we win, and we offer free consultations. Contact us today to talk through your delayed claim with one of our attorneys.

Past results do not guarantee future outcomes.

Insurance Payout Deadline FAQs

Can I file a complaint with the Texas Department of Insurance and still sue my insurer for missing a payment deadline?

Yes. Filing a complaint with the Texas Department of Insurance and pursuing a lawsuit under Chapter 542 are separate actions, and doing one does not prevent you from doing the other. A Texas Department of Insurance complaint can push for faster compliance, while a lawsuit is the path to recovering penalty interest and attorney fees.

Does the 5-business-day payment window apply if the insurer only accepts part of my claim?

Yes. Under Section 542.057, the 5-business-day payment requirement applies to any accepted portion of the claim, not just full acceptance. The insurer must pay whatever it agrees is valid within that window, even while disputing the rest.

What counts as written notice of a claim under Texas law?

Texas courts have accepted certified mail, insurer-portal submissions, and written correspondence as valid written notice, but the exact form depends on your policy language and how the insurer receives it. Verbal reports or phone calls do not start the Stage 1 clock, so always follow up with something in writing and save proof of delivery.

If my insurer denies my claim after the 45-day extension, can I still collect penalty interest?

In certain circumstances. Penalty interest under Section 542.060 applies when an insurer fails to pay a claim that they were obligated to pay, not simply because they denied one. However, if you prove the denial was wrongful, the insurer can owe penalty interest from the date that payment was originally due.

Does the Texas Prompt Payment Act cover commercial or business insurance policies?

Chapter 542 generally applies to first-party insurance claims, regardless of whether the policyholder is an individual or a business. However, certain commercial lines and special policies may not be covered. If your policy is a surplus lines or otherwise exempt type, different rules apply, and you should verify coverage under the statute before assuming those deadlines apply.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...