What Happens If You Miss an Insurance Deadline in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Missing a policy notice deadline rarely voids a claim unless the insurer proves real prejudice.

- CPRC § 16.003 gives Texas injury victims only two years from injury to file a lawsuit.

- Insurers face 18% penalty interest under § 542.060 when they miss prompt-payment deadlines.

You were rear-ended on I-35 near downtown Austin a few weeks ago, and life got in the way. Now you’ve realized you may have missed a deadline that your insurer mentioned in a letter, and panic is setting in. Does this mean your claim is now invalid? The answer depends on which deadline you missed.

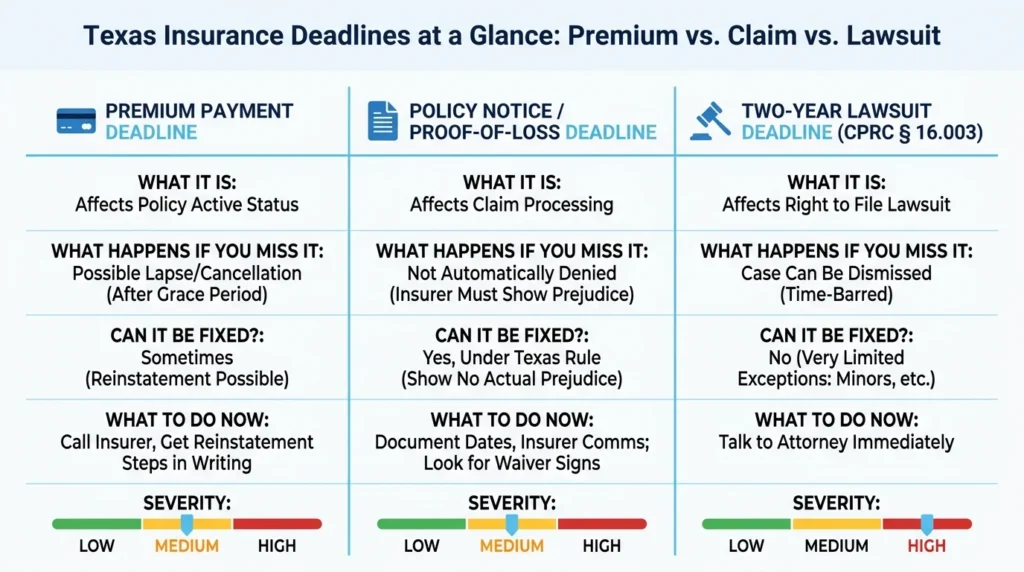

Two Types of Insurance Deadlines in Texas

Not all insurance deadlines work the same way. Missing a premium payment deadline affects whether your policy stays active, while missing a claim filing or notice deadline affects whether your claim survives after a loss. Each carries different legal consequences and different remedies under Texas law.

These two tracks have very different stakes. A late premium might be fixable within days. A missed lawsuit deadline can be permanent. Sorting out which category applies to your situation is the first real step.

Missing a Premium Payment Deadline

A missed premium payment does not always cancel your policy overnight. Texas law and most insurance contracts include a grace period before coverage actually lapses. During that time, your policy stays active and a claim filed in that period is usually still payable, even if you haven’t sent the late payment yet.

For life insurance, the Texas Insurance Code § 1101.005 requires policies to include a grace period of at least one month after a missed due date. Auto and health policies often have grace periods written into the contract itself. Read your policy to see what applies to you.

If the grace period ends without payment, your insurer can cancel the policy. You may still have reinstatement rights depending on the terms and your insurer’s internal rules, so call your insurer the moment you realize a payment was missed. Document the call, ask exactly what’s required to reinstate, and get written confirmation of anything they tell you.

If you need a refresher on how the claims process works after a crash, our guide on how to file a car insurance claim in Texas discusses the basics.

Missing a Claim Filing or Notice Deadline

This is the deadline most people worry about. A missed notice or proof-of-loss deadline is serious but rarely a death sentence for your claim. A missed lawsuit deadline is a different story. Texas treats these two situations very differently, and you need to understand both before you decide what to do next.

Policy-Based Notice & Proof-of-Loss Deadlines

Most Texas insurance policies require “prompt” or “timely” notice of a loss. Proof-of-loss submissions are often due within 30 to 90 days, depending on the policy. Missing these dates does not automatically void your claim.

Texas courts generally require insurers to show they suffered actual prejudice from the late notice before they can deny on that basis alone. If the insurer keeps investigating, asking questions, or communicating with you post-deadline, those actions can support a waiver or estoppel argument.

This means the insurer may have given up the right to use the late notice against you.

Pull your policy and find the exact notice language. Note the date of your loss, the date you reported it, and save every email or letter showing the insurer engaged with the claim. Some readers ask whether a police report is required for insurance claims in Texas when reconstructing this timeline; in most cases, a report helps but isn’t strictly mandatory.

An attorney can review your communications and help determine whether a waiver argument applies before you accept a denial as final.

The Two-Year Statutory Deadline to Sue

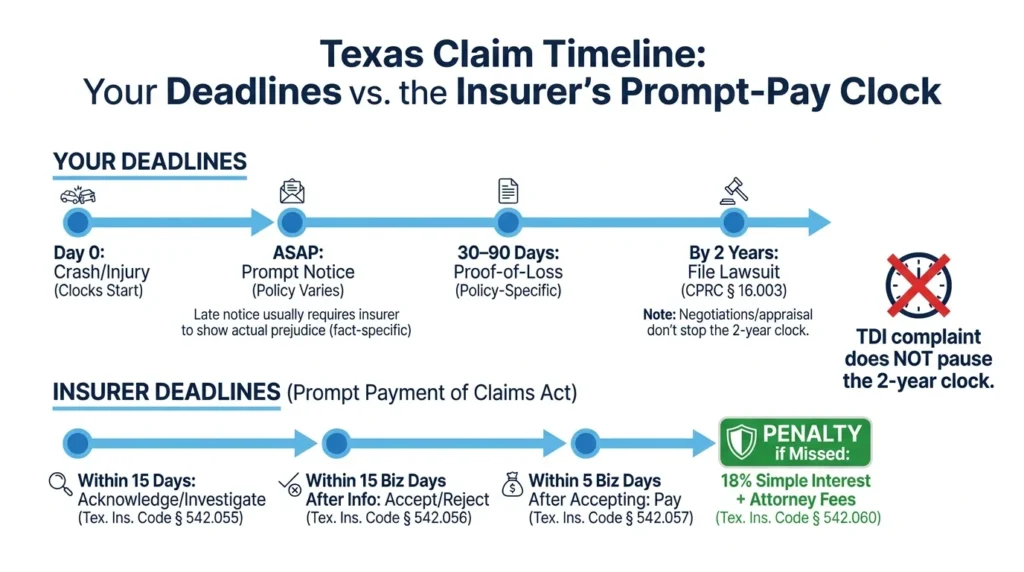

The Texas Civil Practice and Remedies Code (CPRC) § 16.003 gives you two years from the date of injury to file a personal injury lawsuit. This clock runs independently of any insurance notice deadline. It does not pause during claim negotiations, appraisal, or while you wait on the insurer.

Missing this deadline is far more serious than missing a policy notice deadline. Courts dismiss time-barred suits on motion, and the right to challenge is gone. Limited exceptions exist, such as injuries that show up later, tolling for minors, and special rules for claims against government entities. Courts apply these narrowly.

A more detailed breakdown of exceptions to the Texas statute of limitations can help you understand whether any of these might apply.

If the two-year window is upcoming or has just passed, talk to an attorney before assuming nothing can be done. For families dealing with a fatal crash, separate deadlines and rules apply under Texas wrongful death law.

When Your Insurer Misses Its Deadline

Deadlines run both ways. The Texas Prompt Payment of Claims Act puts strict timing rules on insurers once you file a claim. Many people don’t know about these rules until they’ve been waiting weeks for a response.

Under Texas Insurance Code § 542.055, an insurer must acknowledge your claim and begin investigating within 15 days. Once it has all the information it needs, § 542.056 requires it to accept or reject the claim within 15 business days. After accepting, § 542.057 requires payment within 5 business days.

Texas Insurance Code § 542.060 imposes an 18 percent annual interest penalty on unpaid claim amounts when an insurer violates these deadlines, plus liability for your attorney fees. The penalty increases from the date of the violation, running as simple interest until the claim is resolved—a calculation that courts apply through the date of judgment. That’s real leverage.

If you believe your insurer has missed these deadlines, you can file a complaint with the Texas Department of Insurance complaint portal. A pending TDI complaint does not stop the two-year clock on filing suit, so track both timelines side by side. Stalled or denied claims after a wreck are common in car accident cases, and the prompt-pay rules often open doors that appear closed.

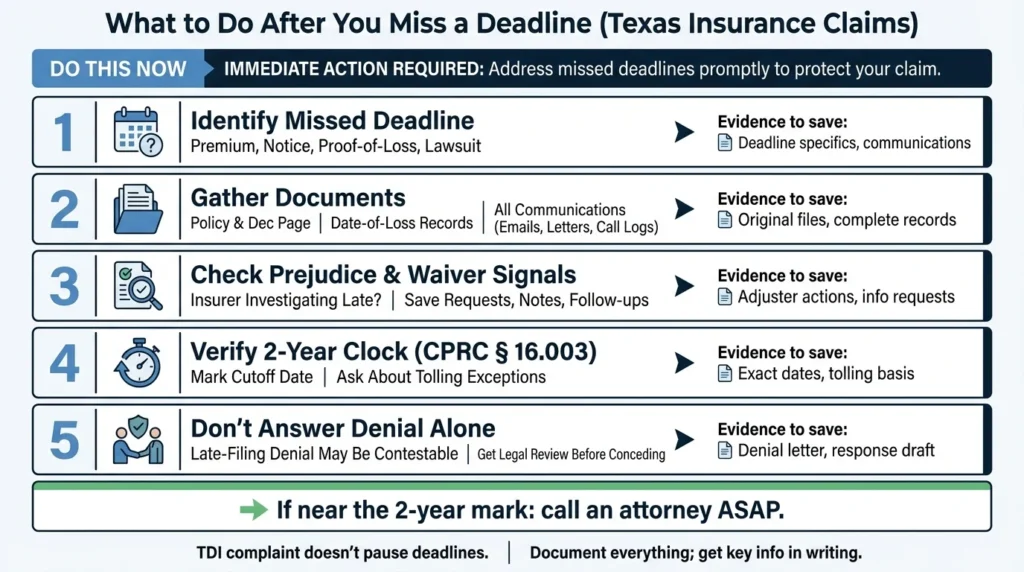

Steps to Take After a Missed Deadline

Take a breath. A missed deadline does not always end your claim, but your next moves matter. Work through these steps in order so you know where you actually stand.

- Identify which deadline you missed. Policy notice, proof-of-loss, and the two-year statute each carry different consequences. Knowing which one applies tells you how much room you have to work with.

- Gather your documents. Pull your policy, the date-of-loss records, every email and letter to and from your insurer, and anything showing the insurer kept working on the claim after the deadline.

- Look at prejudice and waiver. If the insurer wasn’t really harmed by your late notice and kept investigating, those facts help you push back on a denial.

- Check the two-year clock. Inside the window, you can still sue. Outside it, ask an attorney whether any tolling rule applies before you give up.

- Talk to an attorney before responding to a denial letter. A denial citing late filing is not always valid under Texas law.

If the other driver had no coverage, your own policy may step in. Our uninsured motorist accident guide explains how that coverage works and the deadlines tied to it.

Talk to a Texas Insurance Attorney

A missed deadline feels like the end of the road, but it often isn’t. Insurers count on policyholders giving up after a denial letter. Don’t.

Angel Reyes & Associates has represented Texas injury and insurance clients for more than 30 years and reports recovering more than $1 billion for clients. We work on contingency, so there’s no fee unless we win, and we offer free consultations to help you figure out where you actually stand. Contact us today to talk through your situation before assuming your rights are gone.

Past results do not guarantee future outcomes.

Insurance Deadline FAQs

Can I still get my car fixed if my policy lapsed before the accident?

If your policy had already lapsed when the accident happened, coverage does not apply to that loss. A grace period only protects claims that occur while the grace period is still active, not after it has expired.

Does the two-year deadline apply to property damage claims in Texas, too?

Texas law gives you two years to sue for property damage under CPRC § 16.003, the same limitations period that applies to personal injury claims. That clock starts on the date the damage occurred, not the date your insurer denies the claim.

What is a proof-of-loss form and when is it typically due?

A proof-of-loss form is a sworn statement you submit to your insurer documenting the details and dollar amount of your loss. Most Texas policies set a deadline of 30 to 91 days after the loss, but the exact window depends on your specific policy language.

Can I reopen an insurance claim in Texas after I accept a settlement?

Signing a release typically closes the claim permanently, so reopening it afterward is very difficult. If you have not yet signed a release, the claim may still be negotiable even if you accepted a partial payment.

Does filing a TDI complaint pause any deadlines on my claim?

A complaint filed with the Texas Department of Insurance does not toll the two-year statute of limitations or any policy-based deadline. You must track all legal and contractual deadlines separately while your complaint is under review.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...