Does UM/UIM Coverage Apply to Bicycle vs. Vehicle Collisions?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas UM/UIM coverage follows the named insured as a person, even when riding a bicycle.

- UM pays when the driver has no insurance; UIM pays when their limits fall short of damages.

- Under § 1952.104, hit-and-run UM claims usually require physical contact with the unknown vehicle.

You were riding home along the Katy Trail near Uptown when a driver drifted across the bike lane and clipped your rear wheel. The driver stopped just long enough to admit they had let their insurance lapse, then drove off. Now the medical bills are stacking up, and you’re reviewing your own auto policy wondering if it can help when you weren’t even in a car.

UM/UIM Coverage in Texas: What Cyclists Need to Know

Yes, your own auto insurance can cover you as a cyclist. Texas requires insurers to offer uninsured and underinsured motorist (UM/UIM) coverage, and that coverage follows you as a person. If you carry UM/UIM on your auto policy, it can apply when you’re hit while riding a bike, walking, or doing anything else off the road.

The rule comes from Texas Insurance Code § 1952.101, which requires insurers to offer UM/UIM coverage with every Texas auto policy — coverage that applies unless the named insured rejects it in writing. Most drivers don’t reject it, which means most drivers already have this coverage in place.

Texas courts have backed this up for decades. The named insured does not have to be occupying a covered vehicle to trigger UM benefits. Household members listed on the same policy usually get the same protection.

The real question with a cyclist claim isn’t what you were doing when you got hit. It’s whether the driver who hit you was uninsured or underinsured. That’s the threshold that opens the door to your own coverage.

UM vs. UIM: Which Coverage Applies to Your Bike Crash?

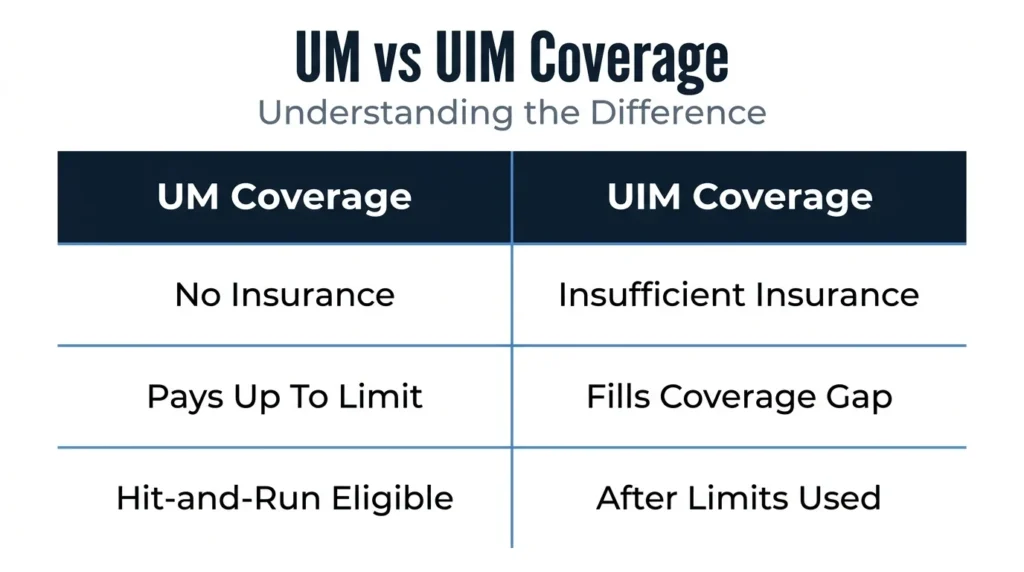

UM and UIM sound alike and are usually sold together, but they apply to different conditions. Knowing which one fits your situation is important because each follows a different claims path. UM responds when the at-fault driver has no insurance at all. UIM responds when they have some, but not enough to cover your damages.

Uninsured Motorist Coverage

UM applies when the driver who hit you had no liability insurance, or when they fled the scene and cannot be identified. It can pay for your medical expenses, lost wages, and pain and suffering up to your UM policy limits.

Hit-and-run cases come with one wrinkle. Under Texas Insurance Code § 1952.104, most policies require physical contact between the unknown vehicle and you or your bike. If the driver swerved and you crashed without being touched, the UM claim gets harder. Document any contact, paint transfer, or damage to your bike right away.

Underinsured Motorist Coverage

UIM applies when the at-fault driver has liability insurance, but their limits run out before your damages are fully paid. Texas Insurance Code § 1952.103 defines when a vehicle counts as underinsured for this purpose.

Here’s how the math usually works. The at-fault driver’s liability carrier pays first, up to their policy limit. Your UIM carrier then steps in to cover the gap between that payout and your full damages, up to your UIM limit. You cannot collect twice for the same loss, but you can close the gap.

The “Occupying” Policy Language Problem

This is where insurers push back. Some auto policies define covered incidents using “occupying” language, meaning in, on, getting into, or getting out of a covered vehicle. Adjusters sometimes use that phrase to argue a cyclist’s claim doesn’t qualify.

Texas law does not support that reading. UM/UIM coverage attaches to the named insured as a person, not to the act of being inside a car. A denial that leans on occupancy language is a legal dispute, not a final answer.

If you get a denial letter, ask the insurer to put the basis in writing. Compare it against the definitions section of your own policy. The language often does not say what the adjuster claims it says.

An attorney can review the policy and the denial together to see whether the insurer’s position holds up under Texas law. For coverage questions tied to a bike crash specifically, our Texas bicycle accident team handles these disputes.

Steps to Take After a Bike Crash with an Uninsured Driver

What you do in the first hours and days shapes your claim. UM/UIM carriers evaluate documented damages, not what you say happened. Build the record while it’s fresh.

- At the scene: Photograph the driver’s vehicle, plates, injuries, your bike, and the surrounding area. Get the driver’s insurance information or note its absence. Collect names and numbers from any witnesses.

- Call the police. A crash report creates an official record of the driver’s uninsured status, which directly supports a UM claim later.

- Notify your auto insurer promptly. UM/UIM policies contain contractual notice deadlines, and delay can complicate or even void coverage.

- Preserve medical records. Get treatment the same day if possible, and keep every bill, scan, and discharge note from that point forward.

- Be careful with recorded statements. Your own UM/UIM insurer is adversarial in these claims. Understand your rights before giving one.

If you carry coverage on more than one vehicle or live with other policyholders, stacking rules may increase what you can recover.

Talk to a Texas Bicycle Accident Attorney

A UM/UIM denial is rarely the end of the story. Texas law gives cyclists real coverage rights, and pushing back on a bad denial often takes legal help. Acting before contractual notice deadlines run is critical.

Angel Reyes & Associates has over 30 years of experience handling personal injury and uninsured motorist claims across Texas, with more than $1 billion recovered for clients. We work on contingency, meaning no fee unless we win, and offer free consultations. You can review our past case results or contact us today to discuss your bicycle crash.

Past results do not guarantee future outcomes.

FAQs Regarding Bicycle vs. Vehicle Collisions

Can I use UM/UIM coverage from a family member's auto policy if I don't own a car?

You may qualify as a resident relative under a household member’s policy, which could extend UM/UIM protection to you even if you are not the named insured. Policy definitions vary, so check the resident relative language in the specific policy.

Does health insurance pay first, or does UM/UIM pay first, after a bicycle crash?

In Texas, health insurance and UM/UIM coverage coordinate rather than duplicate payment, and the order depends on your policy language and any applicable coordination of benefits clauses. Your health insurer may also assert a subrogation lien against your UM/UIM recovery for expenses it already paid.

Will filing a UM/UIM claim after a bike crash raise my auto insurance rates in Texas?

Texas law does not bar insurers from considering UM/UIM claims when setting premiums, though many insurers treat them differently than at-fault accident claims. Reviewing your policy’s surcharge disclosure or asking your insurer directly before filing can help you understand the risk.

Is there a deadline to file a UM/UIM claim after a bicycle accident in Texas?

Texas has a four-year statute of limitations for contract claims, which generally governs UM/UIM disputes with your own insurer, but your policy may contain shorter contractual notice or suit deadlines that apply sooner. Missing either deadline can bar your claim entirely.

Can a cyclist recover for bicycle damage, not just personal injuries, under UM/UIM coverage?

UM/UIM coverage in Texas is designed to compensate for personal injury losses such as medical bills, lost wages, and pain and suffering, and it typically does not extend to property damage like a destroyed bicycle. A separate uninsured motorist property damage endorsement, if purchased, would cover that loss instead.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...