What Does the MCS-90 Endorsement Mean in a Texas Truck Accident Case

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- The MCS-90 is a federal endorsement on interstate carrier insurance policies that overrides common exclusions and requires payment up to the federal minimum amount.

- Coverage floors are $750,000 for general freight, $1,000,000 for hazardous materials, and $5,000,000 for extremely hazardous materials.

- The endorsement only applies to interstate carriers. Carriers that operate only in Texas are not required to carry it.

When a trucking company’s insurer denies coverage after a crash (such as by claiming an exclusion in the policy applies, a vehicle wasn’t listed, or coverage lapsed), the claim does not necessarily have to end there. Federal law built a protection for exactly this scenario: the MCS-90 endorsement. Understanding what it is and when it applies can be the difference between a denied claim and a forced payment.

What Is the MCS-90 and Why Does It Exist?

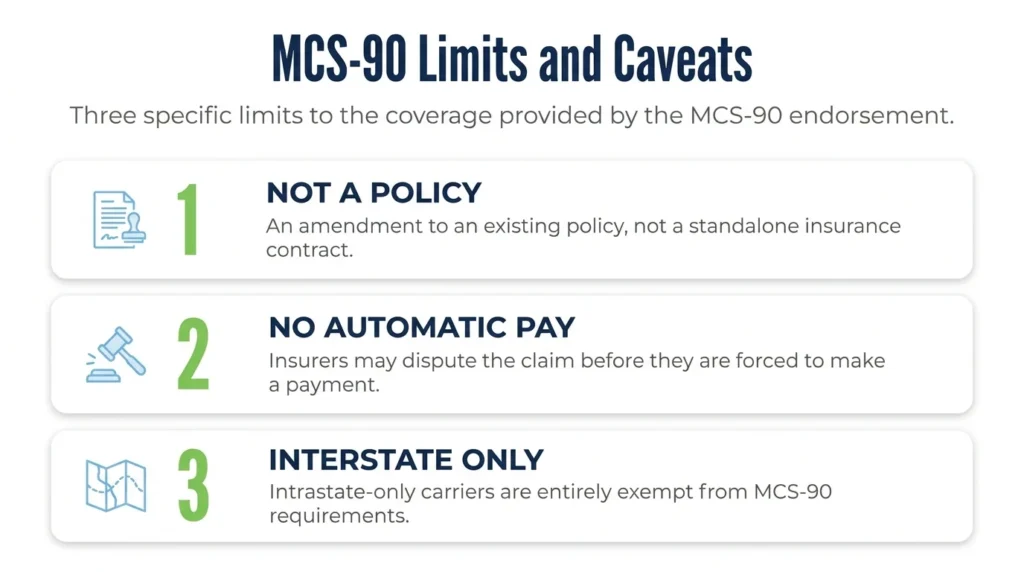

The MCS-90 is a federal endorsement that must be attached to the liability insurance policy of every interstate commercial motor carrier under 49 CFR Part 387. It is not a separate insurance policy. It is an amendment to the carrier’s existing commercial auto liability coverage that adds a federal guarantee on top of whatever the policy says.

Congress required the endorsement because insurers were using standard policy exclusions and technical excuses to deny coverage to crash victims, even when the carrier was clearly responsible. The MCS-90 prevents insurers from doing this (up to the required federal minimum coverage amount). If the carrier’s insurer tries to deny your claim based on a policy exclusion, the MCS-90 requires the insurer to pay regardless.

The endorsement applies only to interstate carriers operating across state lines or under FMCSA authority. Carriers that operate exclusively in Texas are not required to carry the MCS-90 and are instead governed by Texas state rules.

For a broader look at Texas commercial truck insurance requirements, see our blog on Texas commercial truck insurance requirements.

What Exclusions Does the MCS-90 Override?

The most important thing to understand about the MCS-90 is which excuses or legal defenses it stops insurance companies from using. If the carrier’s insurer has denied your claim or threatened to deny it, you must first identify whether the denial falls into one of these categories:

- Unlisted vehicle: In this instance, the insurer argues that the specific truck involved in your crash was not listed or scheduled on the policy. The MCS-90 overrides this exclusion.

- Unauthorized driver: In this instance, the insurer claims that the driver was not an approved or listed driver under the policy. The MCS-90 overrides this exclusion.

- Route or cargo deviation: In this instance, the carrier was hauling a type of cargo or traveling a route that was outside the policy’s scope. The MCS-90 overrides this exclusion.

- Policy lapse: In this instance, the carrier’s premiums were not paid, and coverage was technically suspended at the time of the crash. The MCS-90 overrides this exclusion and requires payment anyway.

- Carrier misrepresentation: In this instance, the carrier provided false information when the policy was originally issued, which gives the insurer grounds to deny coverage. The MCS-90 overrides this exclusion.

In every one of these scenarios, the insurer must pay up to the required federal minimum. The policy exclusion still exists, but after paying the claim, the insurer has the right to pursue reimbursement from the carrier for any payment it made because of an exclusion that would have normally applied. That dispute is between the insurer and the carrier. As the injured party, it is not your problem.

For a closer look at how insurers use these defenses, see how trucking companies and insurers delay and deny claims in Texas.

MCS-90 Coverage Limits

The MCS-90 guarantees payment up to the federal minimum required limits, which depend on what the truck was hauling:

- $750,000 for general freight (non-hazardous property)

- $1,000,000 for oil and certain hazardous materials

- $5,000,000 for certain extremely hazardous materials

These are minimums, not maximums. If the carrier’s policy provides higher limits, and the insurer is not contesting coverage on higher amounts, the MCS-90 is not the main issue. The endorsement is most relevant when the insurer tries to deny coverage entirely. In this situation, it forces the insurer to pay at least the required minimum amount, but it does not increase the maximum coverage limit.

The MCS-90 covers only third-party bodily injury and property damage. It does not apply to the carrier’s own equipment, cargo damage, or the driver’s own injuries. For context on what recoveries in serious 18-wheeler accidents look like, see the average payout for an 18-wheeler accident in Texas.

Does the MCS-90 Apply to Your Claim?

The first step is determining whether the carrier is an interstate carrier who is subject to FMCSA rules. Interstate carriers are required to file proof of insurance with FMCSA, and their filings (including the MCS-90 endorsement) are publicly accessible through the FMCSA SAFER database, searchable by carrier name or USDOT number.

If the insurer tries to deny coverage defense after your crash, the MCS-90 should be reviewed immediately. Identifying the endorsement, confirming it is on file, and using it to challenge the insurer’s denial is part of an early coverage investigation in any serious truck accident case.

For a step-by-step look at how a Texas truck accident claim unfolds, see how truck accident claims work in Texas.

Talk to a Lawyer About Your Truck Accident in Texas

When an insurer denies a truck accident claim based on a policy exclusion, the answer is not always to accept the denial. Federal law may require the insurer to pay regardless, but using the MCS-90 effectively requires that you know whether the endorsement is on file, which exclusion the insurer is using, and how Texas courts have applied the endorsement in similar disputes.

Angel Reyes & Associates has handled truck accident cases across Texas for over 30 years. The firm has recovered more than $1 billion for clients and offers free consultations with no fees unless we win your case. If your claim has been denied, or coverage is being disputed after a truck accident, contact the firm today.

Past results do not guarantee future outcomes.

MCS-90 Endorsement FAQs

What happens if the trucking carrier goes bankrupt after the crash?

The MCS-90 requires the insurer to pay, as well as the carrier. If the carrier goes bankrupt, the insurer still must pay up to the federal minimum under the endorsement. After paying, the insurer can try to get reimbursed by the carrier, but the reimbursement claim may be worthless if the carrier is bankrupt. In this case, the insurer absorbs the loss. The MCS-90 was designed to ensure that victims can still recover compensation, even if the carrier goes bankrupt.

Does the MCS-90 cover accidents in which the driver was at fault but not the carrier?

Yes. The MCS-90 can still require the carrier’s insurance company to pay, even if the trucking company was not directly responsible. It does not hold the driver personally responsible, but you still have to prove who caused the crash. The endorsement removes certain insurance exclusions, but it does not remove the requirement to prove fault.

How long does it take for the MCS-90 to force payment?

The MCS-90 does not guarantee immediate payment. It overrides exclusions that an insurer might otherwise use to deny a final judgment or settlement. Using the endorsement is part of the legal or claim-negotiation process, but it is not an automatic payout. First, the insurer may deny coverage based on an exclusion, and the MCS-90 is your legal basis for challenging their denial. The timeline depends on how aggressively the insurer disputes the claim.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...